(M4E8) [Microeconomics] Consumer Surplus: Compensating and Equivalence Variations

TLDRIn this final episode, the speaker explains consumer surplus, a key concept in applied economics. They discuss how policies impact consumer welfare, how to measure welfare using consumer surplus, and introduce compensating variation (CV) and equivalent variation (EV). The session delves into demand curves, comparing Marshallian and Hicksian demand, and concludes that the Marshallian demand curve offers a reasonable method to calculate consumer surplus. The speaker also covers expenditure minimization and utility levels, providing a comprehensive understanding of consumer welfare analysis.

Takeaways

- 📊 Consumer surplus is a crucial concept in applied economics, helping to measure consumer welfare under different policies.

- 🔍 Consumer surplus is the area between the price line and the demand curve, representing the benefit consumers receive from purchasing goods at a lower price than they are willing to pay.

- 🧮 To measure consumer surplus, compare the area under the demand curve before and after a price change.

- 📈 The demand curve can be viewed as either compensated (Hicksian) demand or Marshallian demand, each offering different perspectives on consumer behavior.

- 📉 Compensated demand (Hicksian demand) maintains a constant utility level, allowing for precise measurement of changes in welfare as prices vary.

- 💸 Marshallian demand reflects changes in quantity demanded based on price and income, without holding utility constant, making it observable in real-world data.

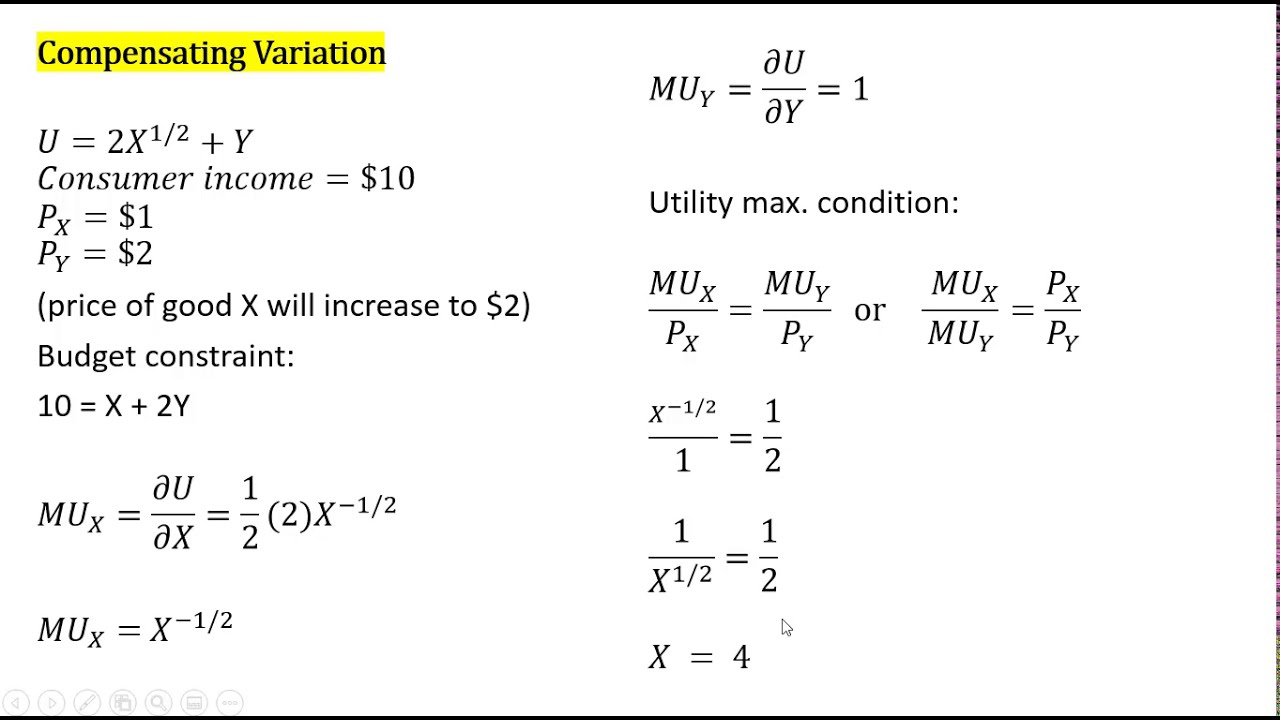

- ⚖️ Compensating Variation (CV) quantifies the amount of money needed to maintain a consumer's initial utility level after a price change.

- 🔄 Equivalent Variation (EV) measures how much a consumer is willing to pay to return to their original situation after a price increase.

- 🔢 Using the Marshallian demand curve to calculate consumer surplus is practical and represents a middle ground between CV and EV methods.

- 🔍 The area between the price lines and the Marshallian demand curve provides an approximate measure of consumer surplus and is commonly used in welfare analysis.

Q & A

What is the main topic discussed in the final episode of the chapter?

-The main topic discussed is consumer surplus, its importance in applied economics, and how it can be measured.

Why is consumer surplus an important concept in applied economics?

-Consumer surplus is important because it helps understand how different policies influence consumers and their welfare in the economy.

How is consumer surplus typically measured?

-Consumer surplus is typically measured by the area between the price line and the demand curve.

What are the two types of demand curves mentioned in the script?

-The two types of demand curves mentioned are compensated demand (Hicksian demand) and Marshallian demand.

What is the difference between Hicksian and Marshallian demand curves?

-Hicksian demand curves are based on compensated demand, which considers changes in utility levels, while Marshallian demand curves are based on observable market prices and income.

What are compensating variation (CV) and equivalent variation (EV)?

-Compensating variation (CV) is the amount of money needed to keep a consumer's utility level the same after a price change. Equivalent variation (EV) is the amount a consumer would be willing to pay to return to their initial situation after a price change.

Why is the area between the price line and the Hicksian demand curve considered the change in consumer surplus?

-This area represents the additional income needed to maintain the same level of utility after a price increase, which is the definition of compensating variation and thus the change in consumer surplus.

How does the script explain the relationship between the Hicksian demand curve and compensating variation?

-The script uses Shepherd's Lemma to show that the Hicksian demand is the partial derivative of the expenditure function, which integrates to the compensating variation, representing the area below the Hicksian demand curve between initial and final prices.

Outlines

😀 Introduction to Consumer Surplus

This paragraph introduces the concept of consumer surplus and its significance in applied economics. The author discusses the measurement of welfare through consumer surplus and explains its basic definition as the area between the price line and the demand curve. The paragraph also touches upon the impact of price changes on consumer surplus and sets the stage for a detailed discussion on the topic.

📈 Comparative Static Analysis and Price Changes

In this paragraph, the author explains the starting point of the analysis, which involves changing the price of a good and observing the resulting demand changes. The paragraph describes how to fix a consumer's utility level and find the minimal expenditure needed to achieve this utility level under different price conditions. The discussion includes solving an expenditure minimization problem and visualizing budget lines and their slopes.

📉 Calculating Changes in Consumer Surplus

This paragraph delves into the practical calculation of changes in consumer surplus using the compensated demand curve and the Shepherd's lemma. The author explains how the area below the compensated demand curve represents the change in consumer surplus and emphasizes the need for integration to derive this measure. The paragraph also discusses the difficulty of observing compensated demand curves and the potential use of Marshallian demand curves as an alternative.

🔍 Understanding Equivalent Variation

The author introduces the concept of equivalent variation, which measures the amount of money a consumer is willing to pay to return to their original situation after a price increase. The paragraph describes how to draw Marshallian and Hicksian demand curves, and how these curves intersect at points where income equals expenditure. The discussion clarifies the differences between initial and final utility levels and their impact on measuring consumer welfare.

🔄 Compensating Variation vs. Equivalent Variation

In this paragraph, the author contrasts compensating variation and equivalent variation, explaining the differences in their calculation and interpretation. The author uses graphical analysis to illustrate how each variation is measured and the implications of choosing one over the other. The paragraph concludes that using the Marshallian demand curve provides a reasonable approximation of consumer surplus by averaging the two variations.

📊 Final Thoughts on Consumer Surplus

The final paragraph summarizes the key concepts discussed, including compensating and equivalent variations and their roles in measuring consumer welfare. The author reiterates the practicality of using the Marshallian demand curve for calculating consumer surplus due to the difficulties in observing Hicksian demand curves. The paragraph wraps up the discussion on demand theory and concludes the episode with a brief farewell.

Mindmap

Keywords

💡Consumer Surplus

💡Applied Economics

💡Demand Curve

💡Compensated Demand

💡Marshallian Demand

💡Compensating Variation (CV)

💡Equivalent Variation (EV)

💡Expenditure Minimization

💡Shepherd's Lemma

💡Utility Function

💡Indirect Utility

Highlights

Consumer surplus is a key concept in applied economics for understanding policy impacts on consumer welfare.

Welfare is measured by consumer surplus, the area between the price line and the demand curve.

The origin

Transcripts

Browse More Related Video

Three Measures of Consumer Welfare: Compensating Variation, Equivalent Variation, Consumer Surplus

Perfect Substitutes Utility: Compensating Variation, Equivalent Variation, and Consumer Surplus

16. Compensating Variation and Equivalent Variation

Y1 8) Consumer and Producer Surplus

Solving for Consumer, Producer, and Social Surplus using Integration

What is Consumer Surplus? | Think Econ | Microeconomic Concepts

5.0 / 5 (0 votes)

Thanks for rating: