Microeconomics- Everything You Need to Know

TLDRThis video script is a comprehensive review for an introductory microeconomics course, covering key concepts and theories essential for success in AP or college-level exams. The instructor guides viewers through the fundamental principles of scarcity, opportunity cost, production possibilities, comparative advantage, and economic systems. The video delves into the intricacies of supply and demand analysis, elasticity, cost curves, and market structures, including perfect competition, monopolies, oligopolies, and monopolistic competition. Additionally, it explores resource markets, market failures, externalities, income inequality, and taxation. With a thorough yet concise approach, this review aims to equip students with the knowledge and skills necessary to excel in their microeconomics studies.

Takeaways

- 😄 The video covers everything needed for an introductory microeconomics course, including concepts like scarcity, opportunity cost, production possibilities curve, and comparative advantage.

- 😃 It explains the fundamentals of supply and demand, equilibrium, elasticity, consumer and producer surplus, and price controls like ceilings and floors.

- 😀 The video dives into the theory of the firm, cost curves (fixed, variable, marginal), and how firms maximize profits in different market structures (perfect competition, monopoly, oligopoly, monopolistic competition).

- 🤔 It discusses the resource market, including the demand for labor, derived demand, minimum wage, and the concept of marginal revenue product (MRP).

- 🙂 The video covers market failures, such as public goods, negative and positive externalities, and income inequality (Lorenz curve and Gini coefficient).

- 😊 It explains different types of taxes (progressive, regressive, and proportional) and their impact on income distribution.

- 😇 The video emphasizes the importance of understanding concepts like producing where marginal revenue equals marginal cost (MR = MC) and the shutdown rule.

- 🥰 It provides a comprehensive review of microeconomic concepts, making it useful for preparing for exams like the AP test or college finals.

- 😍 The video encourages students to practice and identify areas they need to study further, emphasizing the importance of mastering unit 3 (theory of the firm and cost curves).

- 😘 The instructor offers an ultimate review pack with practice questions and additional resources for those interested in further support.

Q & A

What is the main concept covered in Unit 1 of the microeconomics course?

-Unit 1 covers the fundamental concepts of scarcity, opportunity cost, production possibilities curve, and comparative advantage. It introduces the idea of scarcity, which means unlimited wants with limited resources, and opportunity cost, which is the cost of choosing one alternative over another.

How is the production possibilities curve represented, and what does it show?

-The production possibilities curve is a graph that shows the different combinations of producing two goods using all available resources. Any point on the curve is efficient, meaning all resources are being fully utilized. Points inside the curve are inefficient, while points outside the curve are impossible given the current resources.

What is the significance of the shape of the production possibilities curve?

-If the production possibilities curve is a straight line, it indicates constant opportunity costs, meaning the resources required to produce different goods are similar. If the curve is concave to the origin, it means the resources are not very similar, and there is a law of increasing opportunity cost, where producing more of one good requires giving up increasing amounts of the other good.

What is the concept of comparative advantage, and why is it important?

-Comparative advantage is the idea that countries should specialize in producing goods where they have a lower opportunity cost compared to other countries. It suggests that countries should produce and export goods in which they have a comparative advantage and import goods in which they have a comparative disadvantage, leading to mutually beneficial trade.

What is the circular flow model, and what does it represent?

-The circular flow model shows the interactions between businesses, individuals (consumers), and the government in an economy. It illustrates how businesses sell products and buy resources, individuals buy products and sell resources, and the government's involvement through transfer payments, subsidies, and taxes.

What is the law of demand, and what factors influence it?

-The law of demand states that when the price of a good or service increases, the quantity demanded decreases, and when the price decreases, the quantity demanded increases. The factors influencing demand include the substitution effect, income effect, and the law of diminishing marginal utility.

What is the concept of elasticity, and how is it measured?

-Elasticity measures how sensitive the quantity demanded or supplied is to a change in price. It is measured using coefficients such as the elasticity of demand coefficient (percentage change in quantity demanded divided by percentage change in price), cross-price elasticity, and income elasticity. Elasticity determines whether demand or supply is elastic (quantity is sensitive to price changes) or inelastic (quantity is insensitive to price changes).

What is the difference between short-run and long-run cost curves?

-Short-run cost curves assume at least one factor of production is fixed, while long-run cost curves assume all factors of production are variable. In the long run, firms can adjust all inputs, allowing for economies of scale (decreasing average costs) initially, followed by constant returns to scale (stable average costs), and eventually diseconomies of scale (increasing average costs).

What is the rule for profit maximization in perfect competition?

-In perfect competition, firms should produce where marginal revenue (MR) equals marginal cost (MC). This output level maximizes the firm's profits or minimizes its losses. The marginal cost curve is also the firm's supply curve.

What are the main market failures discussed in Unit 6, and how can they be addressed?

-Unit 6 covers public goods, externalities, and income inequality as market failures. Public goods can be provided by the government, externalities can be addressed through taxes or subsidies, and income inequality can be mitigated through progressive taxation or income redistribution policies.

Outlines

🎥 Introduction and Overview

This paragraph introduces the video as a summary and review for an AP or college introductory microeconomics class. It explains that the video will cover key concepts rapidly, not for re-teaching but for final preparation. The narrator mentions an 'ultimate review pack' with additional resources and encourages viewers to support the channel if the videos are helpful.

📚 Foundational Economic Concepts

This paragraph discusses fundamental economic concepts such as scarcity, opportunity cost, production possibilities curve, comparative advantage, terms of trade, and an overview of economic systems like capitalism, command economy, and mixed economy. It also introduces the circular flow model, explaining the interactions between businesses, individuals, and the government.

⚖️ Demand, Supply, and Consumer Choice

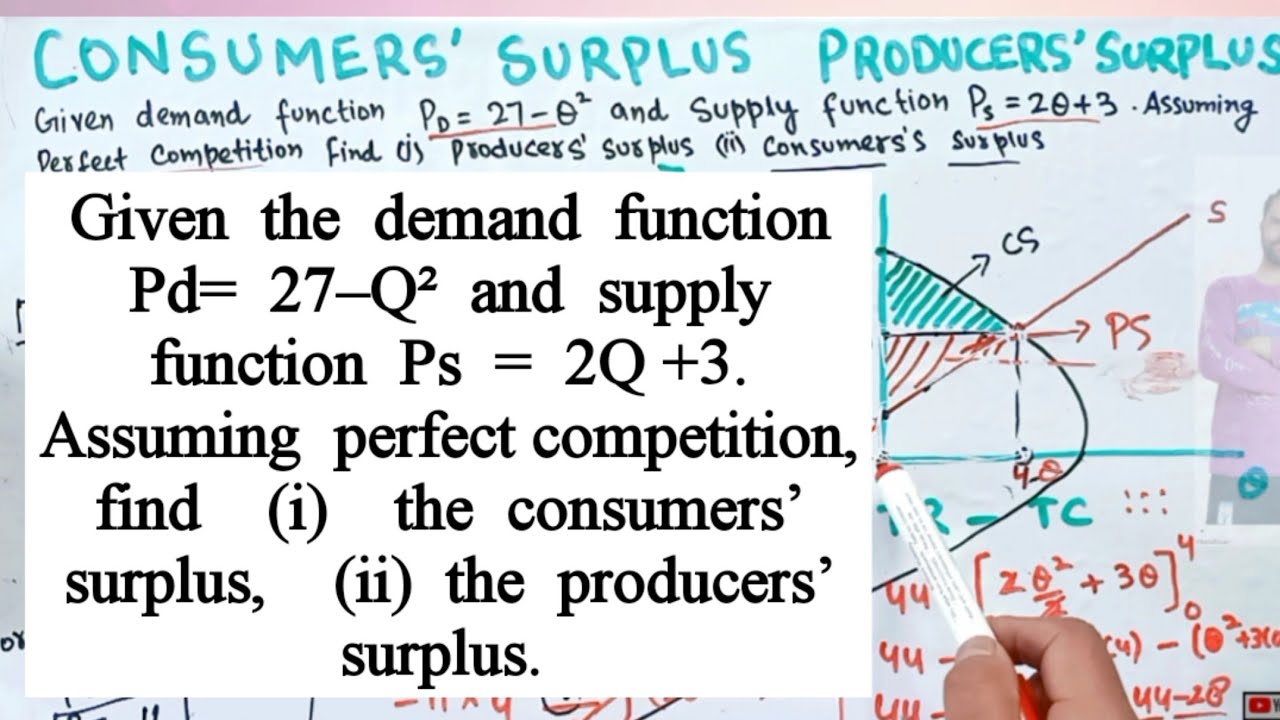

The third paragraph covers the concepts of demand and supply, including the laws of demand and supply, equilibrium, shifts, substitutes and complements, normal and inferior goods, and different types of elasticity (price, cross-price, and income). It also explains the total revenue test, consumer and producer surplus, price ceilings and floors, international trade, taxes and their impact, and the concept of consumer choice using marginal utility.

📈 Costs and Theory of the Firm

This paragraph discusses cost curves (fixed, variable, and total costs), average and marginal costs, and their relationships in the short run and long run. It also introduces the theory of the firm, including perfect competition, profit maximization, the shutdown rule, long-run equilibrium, and the concepts of productive and allocative efficiency.

🏭 Market Structures

The fifth paragraph covers different market structures, including monopolies (natural and price-discriminating), oligopolies, and monopolistic competition. It explains game theory, dominant strategies, and Nash equilibrium for oligopolies, as well as the long-run equilibrium for monopolistic competition.

🔖 Resource Market and Market Failures

This paragraph discusses the resource market, including the derived demand for labor, minimum wage, marginal revenue product (MRP), and the least-cost rule. It also covers market failures, such as public goods, negative and positive externalities, income inequality and the Lorenz curve, the Gini coefficient, and different types of taxes (progressive, regressive, and proportional).

Mindmap

Keywords

💡Scarcity

💡Opportunity Cost

💡Production Possibilities Curve

💡Comparative Advantage

💡Demand

💡Supply

💡Equilibrium

💡Elasticity

💡Costs

💡Theory of the Firm

Highlights

Introduction to AC/DC Econ's comprehensive summary video for AP or college introductory microeconomics.

The purpose of the video is to help students review key concepts right before major tests.

Mention of the Ultimate Review Pack for enhanced learning.

Explanation of scarcity and the concept of opportunity cost.

Introduction to the Production Possibilities Curve and its significance.

Discussion on the Law of Increasing Opportunity Cost.

Insights on how trade can affect a country's Production Possibilities Curve.

Explanation of Comparative Advantage and its importance in trade.

Overview of different economic systems and the Circular Flow Model.

Introduction to demand and supply, including laws and effects.

Explanation of market equilibrium and the impact of price changes.

Discussion on elasticity of demand and its implications.

Introduction to different market structures and their characteristics.

Detailed explanation of perfect competition and its dynamics.

Insight into monopolies, oligopolies, and monopolistic competition.

Discussion on the resource market, including labor demand and supply.

Overview of market failures, public goods, and externalities.

Conclusion with wishes for success on the AP test or final exam.

Transcripts

Browse More Related Video

Macroeconomics- Everything You Need to Know

Consumers' Surplus Producers' Surplus from given Demand and Supply functions

1. Introduction and Supply & Demand

Monopolies and Anti-Competitive Markets: Crash Course Economics #25

Business Optimization and Elasticity!

Revenue, Profits, and Price: Crash Course Economics #24

5.0 / 5 (0 votes)

Thanks for rating: